{kind=link}

Over the previous decade, the room stock of U.S. resort chains has grown extra quickly than that of unbiased inns. Present tendencies point out this progress will proceed as 80.7 % of rooms at present beneath development characterize chains.

In 2010, resort chains accounted for 68 % of the full U.S. room provide. At this time, chains comprise 73 % of the nation’s complete.

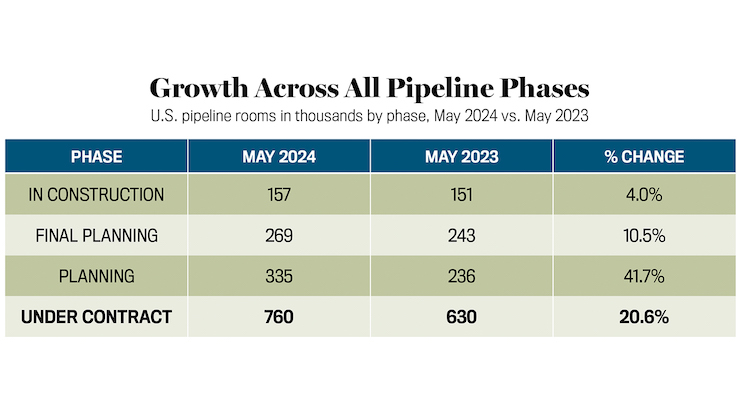

Presently, there are 760,000 resort rooms in numerous phases of planning, remaining planning, or development, marking a 20.6 % improve in comparison with the earlier 12 months. Particularly, the variety of rooms beneath development has risen by 4 %, totaling 157,000 rooms.

STR classifies inns within the pipeline primarily based on their chain affiliation, and solely 19.3 % of rooms in development immediately characterize inns that aren’t recognized with a series. Labeled as unaffiliated for the aim of the pipeline, these rooms are assumed to be unbiased.

Throughout chain sorts, upscale and higher midscale (usually grouped collectively as “choose service”) make up half of the development complete, adopted in descending order by higher upscale, midscale, financial system, and luxurious.

Examination of the full pipeline reveals higher midscale chains and unaffiliated inns making up a better share of complete rooms in comparison with the development part. Meaning there are extra rooms in planning and remaining planning throughout these two segments and fewer rooms in higher upscale and luxurious.

Pipeline exercise throughout the Prime 25 Markets reveals extra exercise amongst unaffiliated properties and upper-level chains. Near 30 % of in-construction rooms are unaffiliated and nearly 35 % are within the planning or remaining planning phases. The nationwide measure, nevertheless, falls to twenty % for the in-construction and planning phases.

Upscale rooms are the second strongest by way of in-construction and general pipeline adopted by higher midscale. Higher upscale posts a pipeline image like america.

Among the many Prime 25 Markets (ranked by in-construction as a share of complete provide), the highest 4 markets current a range by way of the combo of chain and unbiased rooms within the pipeline.

- New York Metropolis tops the record with 7 % of in-construction rooms as a share of current provide. Chains dominate the pipeline available in the market, making up 70 % of rooms in comparison with unaffiliated (30 %).

- Phoenix is the following largest market (5.3 % of in-construction rooms as a % of complete provide) with a 60/40 mixture of chain vs. unbiased rooms within the pipeline.

- Miami, with 4.6 % of provide within the development pipeline, reveals a 48/52 chain/unbiased combine.

- Nashville deviates from the norm with a 97/3 mixture of chain vs. unbiased rooms within the pipeline. In-construction rooms make up 4.5 % of Nashville’s complete provide.

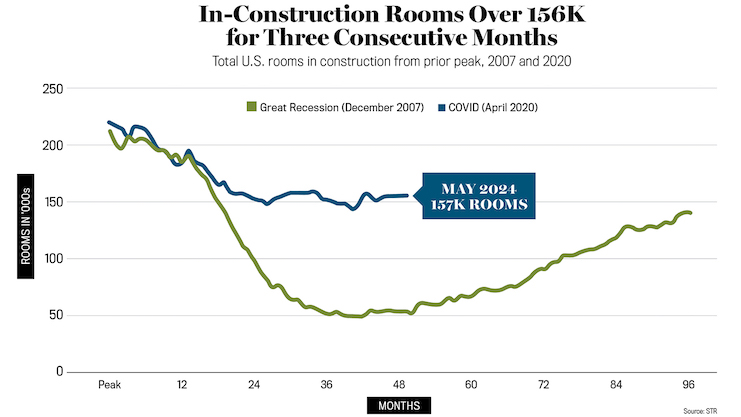

Throughout the nation, resort improvement has returned at a exceptional fee when in comparison with the final downturn. In each this downturn and the final downturn in 2007, the earlier peak exceeded 200,000 rooms, and exercise took roughly three years from the preliminary descent to begin turning up.

Within the final downturn, rooms in development dropped to beneath 50,000 earlier than beginning to improve. At this time, we’re already beginning to see a rise from a degree over 3 times better than what was skilled within the final downturn, with the final three months having remained above 156,000 rooms. With the strong pipeline, hoteliers can anticipate to be challenged with new provide coming on-line and chains having the higher hand.